There are two aspects to property tax relief for homeowners who have suffered total loss or significant damage from the recent fire. The first is to seek an immediate reduction in tax for the period following the fire, due to the property’s decline in value. This will reduce the tax the owner must pay when subsequent installments come due during the period of reconstruction. This reduction will be from the month in which the damage occurred, and will remain in effect until the property is rebuilt or repaired. The second is to consider how rebuilding the home may affect the reassessment of the property after repairs or a complete rebuild is completed.

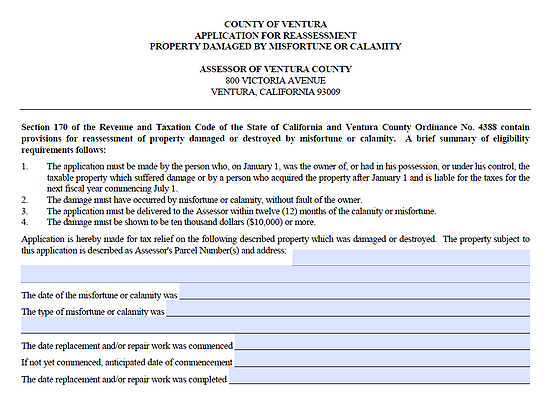

Application for Immediate Reassessment.

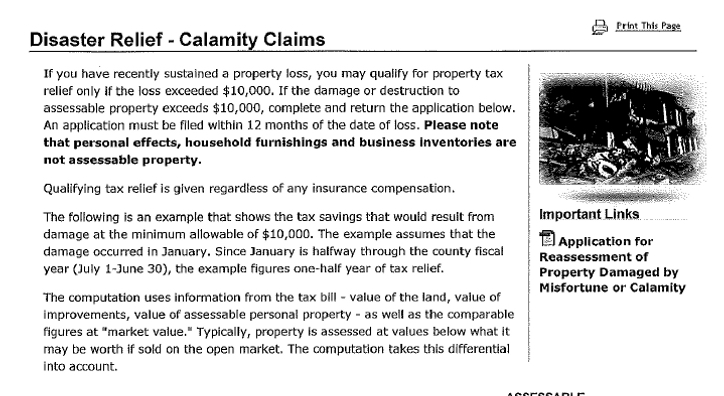

Below is the downloadable form that should be filed with the County Assessor’s Office as soon as possible after the loss occurs. Below is a link to a page on the Assessor website that gives more information and an example of how the property tax reduction is calculated.

http://assessor.countyofventura.org/taxsavings/calamityclaims.html

Reconstruction and Reassessment.

If the home is rebuilt in a like or similar manner, the property will retain its prior value (Proposition 13) for tax purposes. However, any new square footage or extras, such as additional baths, will be added to the base year value at its full market value.

There are two other tax relief provisions that might apply to some homeowners:

Cancellation of Penalty for Late Payment of Tax Installment:

If the homeowner missed the 1st installment of property tax due on December 11th because he/she was a first responder or the property was damaged, a Cancellation of Penalty form can be submitted to the Tax Collector.

Deferral of Future Installment Payments:

A homeowner who has filed a calamity claim for reassessment (above) may apply to the county assessor to defer payment of the next installment of property taxes. If a timely claim for deferral is filed, the payment shall be deferred without penalty or interest until the assessor has reassessed the property and a corrected bill prepared pursuant to Section 170 has been sent to the property owner. Taxes deferred pursuant to this section are due 30 days after receipt by the owner of the corrected tax bill and if unpaid thereafter are delinquent and shall be